An appraisal is crucial for estate planning as well as valuation for tax purposes. It is always best to have an accurate and up-to-date appraisal when any property is involved.

Having a current appraisal helps you keep better track of your financial assets rather than estimating from an outdated appraised value. Properties can often increase in value, and they can decrease just as easily.

ESTATE PLANNING

For estate planning, appraisals can help determine the values of assets. This knowledge is indispensable for heirs if properties and assets need to be gifted or divided after a death.

Keeping an up-to-date appraisal on file is also handy when determining the increase of property value as well as growth or loss margins. Being able to see steady growth or loss over time can help determine proper selling and buying values for good investment opportunities.

ESTATE TAXES

Appraisals are also helpful for estate tax purposes. Having an accurate appraisal can help in the case of a tax audit. Many privately owned businesses are required by the IRS to have an appraisal for determining values if claimed on tax returns.

Appraisal costs are often tax deductible, so check with your tax preparer to determine if that works in your situation.

WE LOOK FORWARD TO ASSISTING YOU IN YOUR APPRAISAL NEEDS. CONTACT US TODAY FOR A PROFESSIONAL AND ACCURATE APPRAISAL.

WE BID EVERY PROJECT. CLICK AN ICON TO LEARN MORE ABOUT OUR APPRAISAL SERVICES.

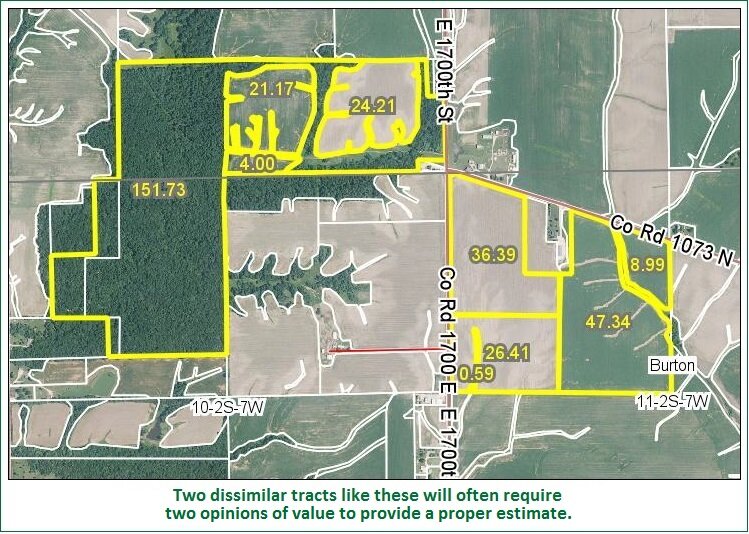

Selections From Our Monthly Newsletter

2032A ESTATE VALUATION

by Mason Spurgeon, Certified General Real Estate Appraiser

April 2018

No one ever wants to deal with the IRS, and they especially don’t want to over-pay them. I remember a funny quote from Ron Paul: “Don’t steal! The Government Hates Competition,” and I know that’s how most of us feel. The IRS is a huge bureaucracy that very few want to question, but with the right help, loopholes within the tax code can be used to reduce your tax burden, legally. One of the ways your tax burden can be reduced is through the 2032A, Special Use Valuation.

The Internal Revenue Code Section 2032A, Special Use Valuation is a valuation method used in figuring the federal taxes for an estate. An appraiser normally values a property according to its fair market value (what the tract would sell for on the open market). However, with a 2032A valuation, the value is based on the property’s current use. This can typically reduce the value of the land and in turn reduce the tax burden. This all sounds great, but with the IRS there are always technicalities.

The first task is making sure that the real estate qualifies for the 2032A Valuation election. There are several rules that dictate if a property applies. The list below summarizes requirements from the IRS website.

The decedent (the person who has died) must be a US citizen.

The real property must be in the United States.

The property must have been used by the decedent or family member for farming in a qualified manner for 5 out of the last 8 years.

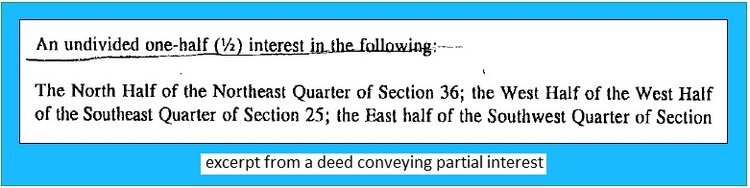

Property must pass to a qualifying heir.

The farm assets, both real and personal, must compose at least 50% of the estate and the real property must compose at least 25% of the total value of the adjusted estate.